AMARILLO, TX – What is the Employee Retention Credit? The Employee Retention Credit (ERC) is a federal tax credit for eligible employers to incentivize them to maintain employees on their payroll. It is not a tax credit available to employees. The ERC provides up to $26,000 tax credit per employee for wages paid from March 2020 until October 2021. The ERC can be claimed retroactively; therefore; it is not too late for employers to claim this credit.

AMARILLO, TX – What is the Employee Retention Credit? The Employee Retention Credit (ERC) is a federal tax credit for eligible employers to incentivize them to maintain employees on their payroll. It is not a tax credit available to employees. The ERC provides up to $26,000 tax credit per employee for wages paid from March 2020 until October 2021. The ERC can be claimed retroactively; therefore; it is not too late for employers to claim this credit.

Relevant Statutes and Regulations

The ERC was originally enacted as part of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) in March of 2020. It was later extended and modified by:

- Taxpayer Certainty and Disaster Relief Act of 2020 (Relief Act)

- American Rescue Plan Act of 2021 (ARPA)

- Infrastructure Investment and Jobs Act of 2021 (IIJA)

Relevant IRS Notices and Guidance

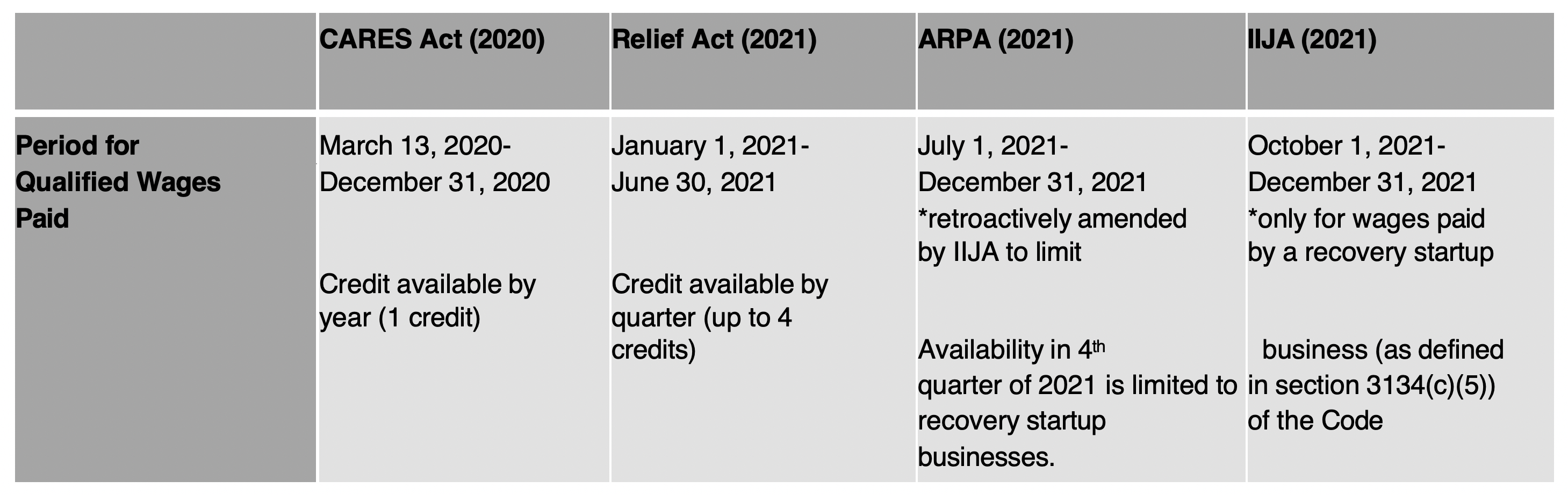

For wages paid after March 12, 2020, and before January 1, 2021:

- Notice 2021-20

- Notice 2021-49

- Revenue Procedure 2021-33

For wages paid after December 31, 2020, and before July 1, 2021:

- Notice 2021-23

- Notice 2021-49

- Revenue Procedure 2021-33

For wages after June 30, 2021, and before October 1, 2021:

- Notice 2021-49

- Revenue Procedure 2021-33

For wages paid after September 30, 2021, and before January 1, 2022:

- Notice 2021-23

- Notice 2021-65

The Basic Who, What, When

Receipt of ERCs is based on several factors:

- time period in which qualified wages are paid;

- whether the employer is an “eligible employer;” and

- impact of COVID-19 on the employer.

How these characteristics are defined evolves with each statute.

Evolution of the ERC: Period for Qualified Wages

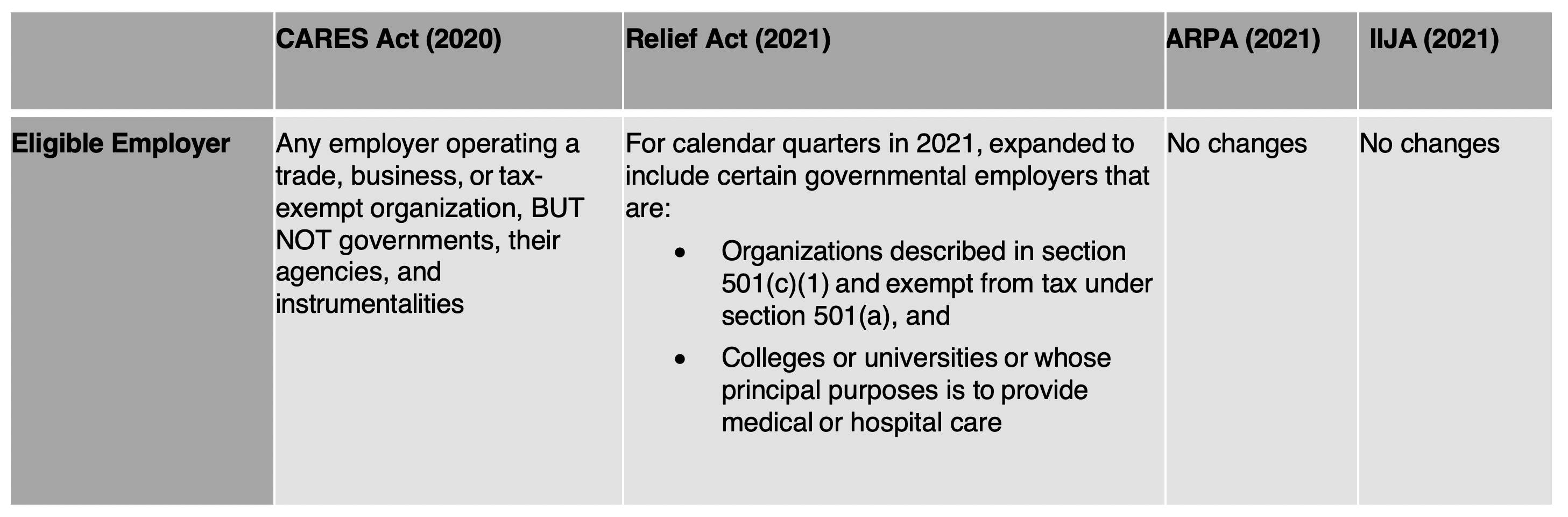

Evolution of the ERC: Eligible Employers

Evolution of the ERC: Eligibility Requirements Under the CARES Act 2020

The employer must experience (i) full or partial suspension of operations due to a government order due to COVID-19 during any quarter or (ii) a significant decline in gross receipts. In order for an employer to satisfy the “significant decline” in gross receipts test in 2020, its gross receipts must fall below 50% of the gross receipts as compared to the same calendar quarter of 2019. If this threshold is met, the employer is eligible “beginning when gross receipts are less than 50% of gross receipts for the same calendar quarter in 2019 and ending in the first calendar quarter after the calendar quarter in which gross receipts are greater than 80% of the gross receipts for the same calendar quarter in 2019.” However, even if an employer does not satisfy the “significant decline” in gross receipts tests in 2020, it may still qualify as an “eligible employer” under the “full or partial suspension of operations” test.

Evolution of the ERC: Eligibility Requirements Under the Relief Act of 2021

For each calendar quarter in 2021, the Relief Act amended the definition of “significant decline” of gross receipts to include any quarter in which the employer’s gross receipts were “less than 80% of the same quarter in 2019.” In other words, as long as an employer’s gross receipts are down by at least 20% compared to the same calendar year in 2019, an employer satisfies the “significant decline” test for that quarter in 2021.

Additionally, “for calendar quarters in 2021, the alternative quarter election rule gives employers the ability to look at the prior calendar quarter and compare it to the same calendar quarter in 2019 to determine whether there was a gross decline in receipts.”

Evolution of the ERC: Eligibility Requirements Under the American Rescue Plan Act of 2021 (ARPA)

Evolution of the ERC: Eligibility Requirements Under the American Rescue Plan Act of 2021 (ARPA)

ARPA applies only to the third and fourth calendar quarters of 2021. ERC is available to “recovery startup businesses” that do not otherwise meet the eligibility criteria, as discussed above. “‘Recovery startup businesses’ are employers that: (i) began carrying on any trade or business after February 15, 2020; (ii) had average annual gross receipts under $1 million for the three taxable-year period ending with the taxable year that precedes the calendar quarter for which the credit is determined; (iii) and do not meet other eligibility criteria (full of partial suspension or decline in gross receipts).”

Evolution of the ERC: Eligibility Requirements Under the Infrastructure Investment and Jobs Act 2021 (IIJA)

Under IIJA, ERCs previously available to all eligible employers for the fourth calendar quarter of 2021 are limited to recovery startup businesses only. For the fourth calendar quarter, “recovery startup businesses” may qualify for ERC even if they are otherwise an eligible employer due to full or partial suspension of operations or a decline in gross receipts.

Claiming the ERC Retroactively

Deadline to Claim

Employers can still claim the ERC for eligible employees for 2020 and 2021 by amending their tax filings. An employer may amend its filings for up to three years after filing or two years after paying, whichever is later. Claims can be filed with respect to unclaimed credits for 2020 until April 15, 2024, and for 2021 until April 15, 2025.

How to Amend Tax Filing to Claim ERC

Employers must file a Form 941X (Adjusted Employer’s Quarterly Federal Tax Return or Claim for Refund). The employer must file a separate Form for each calendar quarter in 2021 for which an employer wishes to claim the credit. Errors or mistakes found can still be reported using the Form. Employers are advised to utilize the help of a tax attorney or CPA to assist them in filling out and filing this Form.

How Much an Employer Can Claim in ERCs

The total value of credit available is based on the number of employees and the wages actually paid to those employees. Maximum credit available varies with the time period in which wages were paid.

The number of employees for which ERC can be claimed is unlimited, unless the employer is a recovery startup business (credit capped at $50,000 per calendar quarter, regardless of number of employees).

Value of Credit Available Under the CARES Act of 2020

For 2020, 50% of qualified wages, capped at a maximum credit of $5,000 per employee for the year, is available. In other words, as long an as employee’s qualified wages were at least $10,000, the employer may claim the full $5,000 in ERC for 2020 for that employee.

Wages considered to be “qualified wages” depends on the number of employees a employer has.

- For employers with “100 or fewer average full-time employees in 2019, wages paid to employees providing services AND NOT providing services are qualified wages.”

- For employers with “greater than 100 average full-time employees in 2019, wages paid to employees NOT providing services are qualified wages.”

Value of Credit Available Under the Relief Act of 2021

For each calendar quarter in 2021, 70% of qualified wages, capped at a maximum credit of $7,000 per employee, per quarter, is available. In other words, as long an as employee’s qualified wages were at least $10,000 in a given quarter in 2021, the employer may claim the full $7,000 in ERC for quarter in 2021 for that employee.

Wages considered to be “qualified wages” depends on the number of employees an employer has.

- For employers with “500 or fewer average full-time employees in 2019, wages paid to employees providing services AND NOT providing services are qualified wages.”

- For employers with “greater than 500 average full-time employees in 2019, wages paid to employees NOT providing services are qualified wages. “

Value of Credit Available Under the American Rescue Plan Act of 2021 (ARPA)

Under ARPA, the maximum ERCs available for Q1, Q2, and Q3 remain unchanged from the maximums implemented by the Relief Act. However, wages that may be considered “qualified wages” are expanded under ARPA for the third and fourth quarters of 2021. “For the third and fourth quarters of 2021, ‘severely financially distressed employers’ may treat all wages as qualified wages during the calendar quarter in which the employer is severely financially distressed. ‘Severely financially distressed employers’ are eligible employers with gross receipts that are less than 10% of the gross receipts in a calendar quarter as compared to the same calendar quarter in 2019.”

This modified definition of qualified wages for severely financially distressed employers applies to employers of all sizes. However, if an employer is not severely financially distressed, but was not in existence in 2019, that employer “may use the 2020 average number of full-time workers to determine whether the employer had greater than 500 average full-time employees” for the purpose of determine which wages paid to employers may be considered qualified wages.

Value of Credit Available Under the Infrastructure Investment and Jobs Act of 2021(IIJA)

Under IIJA, for the fourth calendar quarter of 2021, ERC is available only to recovery startup businesses. If an employer is a recovery startup business, the maximum credit available is capped at 70% of qualified wages per employee for the fourth quarter of 2021. Further, “rules relating to ‘severely financially distressed employers’ are no longer apply in the fourth calendar quarter of 2021.”

Evolution of the ERC: Employment Tax Offset

Additional Considerations

The ERC cannot exceed the payroll taxes withheld from employees’ paychecks. Any excess amounts can be carried forward to a future quarter. Employers should check with their state’s Department of Revenue for additional requirements or restrictions regarding the ERC. The ERC is not considered taxable income. This means employees will not have to pay additional taxes on wages the ERC covers. For employers, the ERC is treated as a business expense that can be used to offset taxes owed.

Common Pitfalls

Common pitfalls include (i) incorrectly counting the average full-time employees and (ii) improper aggregation of employees (parent-subsidiary, brother-sister, affiliated groups, and so on). Business owners are prohibited from filing for the ERC on wages paid to relatives of a majority equity owner of a business. The IRS has reminded employers that improper filing and amendments may lead to fines, clawbacks, and other penalties.

Other common pitfalls include:

- Impermissible “double dipping” coverage of PPP loans and the ERC.

- Overapplication of the supply chain impact on operations. Supply chain argument may provide for eligibility only if (i) the supplier is S.-based; (ii) the supplier is under a full or partial suspension due to a domestic COVID executive order; and (iii) the supplier’s full or partial suspension is causing the business operations to experience a more than nominal effect.

- Misunderstanding and misapplication of “partial suspension” of

For an employer to be eligible under the “partial suspension” test, business operations subject to modifications due to a COVID governmental order, and the actual effect of those modifications, must be “more than nominal.” Unfortunately, the IRS does not define “nominal.”

Employer Beware: Scammers on the Rise

The IRS has issued warnings to employers to beware of third parties promoting improper ERCs. The ERC is complicated, and ill-informed or malicious third parties are taking advantage. Some third-party providers (“ERC Mills”) are guaranteeing businesses a refund without fully understanding the employer’s circumstances. The employer retains ultimate responsibility for proper filing and amending of taxes.

Third parties may not be aware of the common pitfalls discussed in this article. Third parties may neglect to inform businesses that wage deductions reported on the companies’ federal income tax returns must be adjusted to account for the credit amount. Employers should cautiously approach advertised schemes or direct solicitations that promise excessive tax savings, especially those that promise such savings without examining the employer’s records to determine eligibility. Incorrectly claiming the ERC may result in the credit being repaid plus penalties and interest.

Jeffrey S. Baird, JD, is chairman of the Health Care Group at Brown & Fortunato, PC, a law firm with a national health care practice based in Texas. He represents pharmacies, infusion companies, HME companies, manufacturers and other health care providers throughout the United States. Mr. Baird is Board Certified in Health Law by the Texas Board of Legal Specialization and can be reached at (806) 345-6320 or [email protected].

Kianna L. Sitarski, JD, is an attorney with the Health Care Group at Brown & Fortunato, PC, a law firm with a national health care practice based in Texas. She represents pharmacies, infusion companies, HME companies, manufacturers and other health care providers throughout the United States. Ms. Sitarski can be reached at (806) 345-6338 or [email protected].